US-China Trade Breakthrough at APEC: What the October Deal Means for Industrial Investment in India

The Deal That Changed Everything: October 30, 2025 Trump-Xi Agreement

Trade tensions between the United States and China reached a critical juncture in October 2025, but the story took an unexpected turn. After months of escalating tariff threats and market uncertainty, President Trump and Xi Jinping met at the APEC Summit in Busan, South Korea, on October 30, 2025 and reached a breakthrough agreement.

Rather than triggering the threatened 100% tariffs that had spooked global markets just weeks earlier, both nations stepped back from the brink and negotiated a tactical de-escalation that provides temporary stability, but with a critical expiration date looming.

For companies operating in global supply chains and particularly for investors in industrial real estate and logistics

infrastructure, this deal represents both an opportunity window and a strategic test.

Here's what you need to know about the agreement, what it means for trade patterns and why it matters for industrial land investment in India and specifically Tamil Nadu.

What Actually Happened at Busan: The October 30 Agreement Explained

The Trump-Xi meeting in Busan produced a concrete agreement with specific terms, not the vague "ceasefire" some feared:

The Critical Detail:

All major provisions expire on November 10, 2026 exactly 12 months from the agreement. This creates a defined

planning window for companies and investors, but also a known point of potential re-escalation.

Understanding the Trade Data: Beyond the Headlines

To make sense of this agreement, you need to understand the trade dynamics that led to October's tensions. The popular narrative suggests China is "winning" while the US struggles, but the real picture is more nuanced and reveals important patterns for investors.

China's Export Engine: Resilient But Volatile

Despite rising tariffs and geopolitical strain, China's export sector remained remarkably resilient through 2025. For the January-August 2025 period, China's total exports grew approximately 3.5% year-on-year in yuan terms. But this headline number masks profound monthly volatility:

Export Growth Pattern (Jan-Oct 2025):

January: 2.3% YoY growth

February: 5.1% YoY growth

March: 12.4% YoY growth (Front-loading surge before tariff hikes)

April: 8.1% YoY growth (Normalization)

May: 6.2% YoY growth

June: 4.8% YoY growth

July: 3.5% YoY growth

August: 1.2% YoY growth

September: 0.1% YoY growth

October: -1.1% YoY growth (Contraction)

What the Pattern Shows:

Companies front-loaded shipments ahead of anticipated April tariff increases, then gradually normalized as tariff impacts materialized. By October, even before the October 30 deal, exports fell as market pessimism set in.

This volatility reflects a critical trend: China's diversification strategy is working. Rather than relying solely on US

markets, Chinese exporters have successfully redirected shipments to alternative markets.

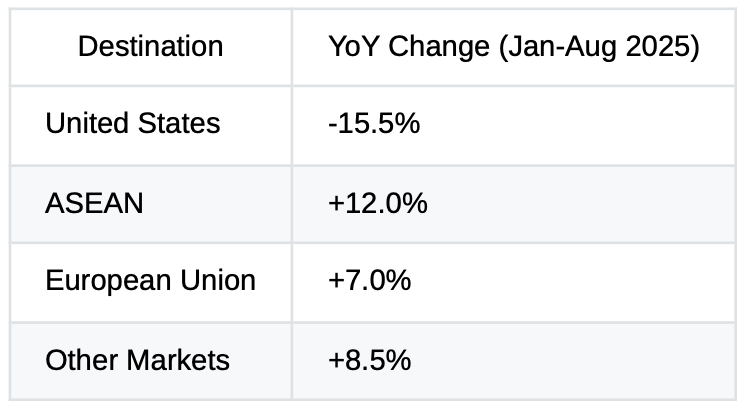

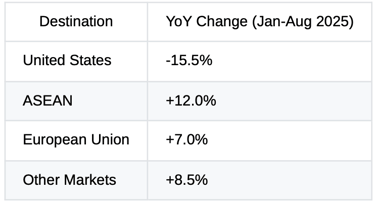

Export Diversification: The Real Story

From January to August 2025, while US-bound exports plunged, shipments to alternative markets surged significantly:

What This Means:

China's share of US imports fell from 17.5% (2019) to 13.8% (2024)

This represents a structural reordering of global trade, not just a temporary adjustment

Alternative suppliers (Mexico, Vietnam, India, ASEAN) have captured the gap

China's exports have successfully pivoted rather than contracted

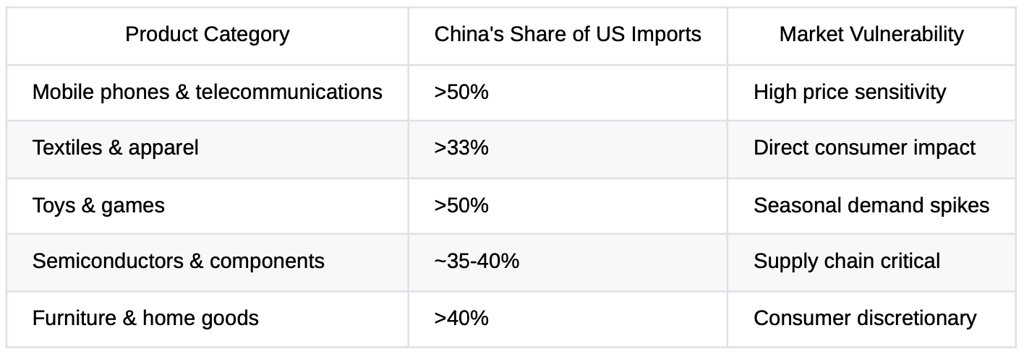

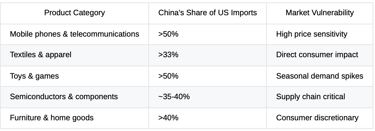

US Import Dependency: Still Concentrated But Shifting

While overall import concentration from China has decreased, the United States remains highly dependent on Chinese suppliers in specific categories:

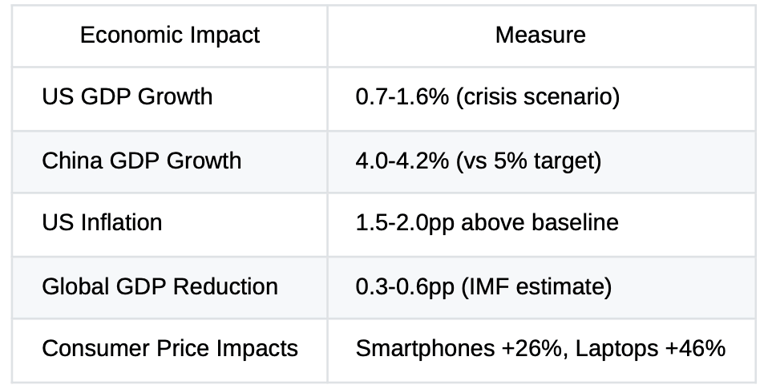

This dependency means that while the October deal reduces immediate tariff risk, any future escalation would directly impact US consumer prices in these categories. Economic modeling shows:

100% tariffs on smartphones: +26% consumer price increase

100% tariffs on laptops: +46% consumer price increase

Overall CPI impact: 1.0-1.5 percentage point increase

Tariff Trajectory: Current Reality vs Future Scenarios

The October agreement achieved a significant reduction, but the path forward remains uncertain:

Tariff Rate Scenarios:

Pre-October Peak: 57%

Post-October Deal (Current): 47%

Renewed Escalation (2026): 60-75%

Full Trade War (2026): 145%

Key Insights:

Current Status (Nov 2025): Tariffs at 47% represent a 10-point reduction from October's 57% peak

Base Case (2026): Agreement extensions maintain ~47% rates

Renewed Escalation: If negotiations fail, tariffs could climb to 60-75%

Full Trade War: Return to all threatened tariffs pushes combined rates above 145%

The Three Paths Forward: What Happens When the Deal Expires?

The October 30 agreement buys time, but it doesn't resolve underlying tensions. Investors must prepare for three distinct scenarios over the next 12-18 months:

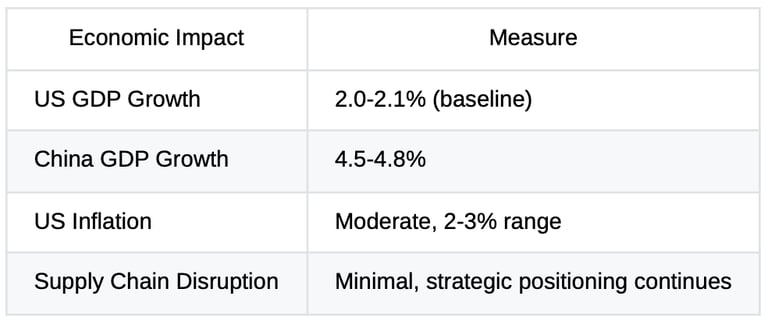

Scenario 1: Base Case — Managed Stability (Most Likely, ~60% probability)

Agreement Terms: Extended or replaced with more permanent framework in October 2026

Tariff Status: Remain at approximately 47% with gradual sectoral negotiations

China's Position: Maintains rare earth export restraint, continues diversifying to ASEAN/EU

Industries Most Affected: Electronics, automotive, machinery, textiles benefit from predictable tariff environment

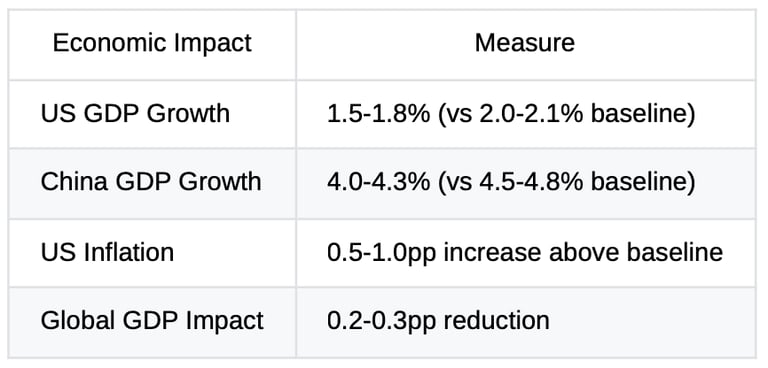

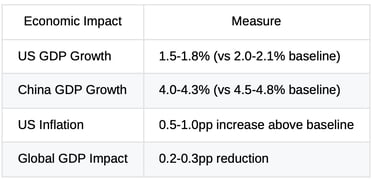

Scenario 2: Renewed Escalation — Gradual Deterioration (~25% probability)

Trigger: Agreement provisions expire without extension in November 2026

Tariff Path: Increase from 47% to 60-75%

China's Response: Reinstates rare earth export controls with expanded scope, targets US technology/EVs

Supply Chain Effect: Accelerated diversification to ASEAN, Mexico, India at higher cost

Scenario 3: Full Escalation — Trade War Reset (~15% probability)

Trigger: Breakdown of October agreement and return to confrontational policies

Tariff Peak: US imposes 100% additional tariffs; combined rates exceed 145%

China's Response: Retaliates with 100-125% tariffs on US goods

Supply Chain Effect: Critical shortages in electronics, semiconductors, rare earths; costly emergency reshoring

Why This Matters for Industrial Land Investment in India and Tamil Nadu

Here's where this trade story becomes directly relevant to industrial investment. The US-China trade reconfiguration is not just a macroeconomic abstraction, it's creating concrete, measurable demand for industrial real estate and logistics infrastructure across India, particularly in Tamil Nadu.

The Supply Chain Realignment Imperative

Multinational corporations are pursuing a deliberate "China+1" strategy. This means:

Maintaining 60-70% production in China for cost efficiency

Diversifying 30-40% production to alternative locations

India has emerged as the primary beneficiary

Target Sectors for Relocation:

Electronics & semiconductors (PLI subsidies up to 6% on capex)

Automotive & EV components (government support for assembly)

Textiles & apparel (high tariff exposure driving urgency)

Logistics & warehousing (growing bottleneck as trade diversifies)

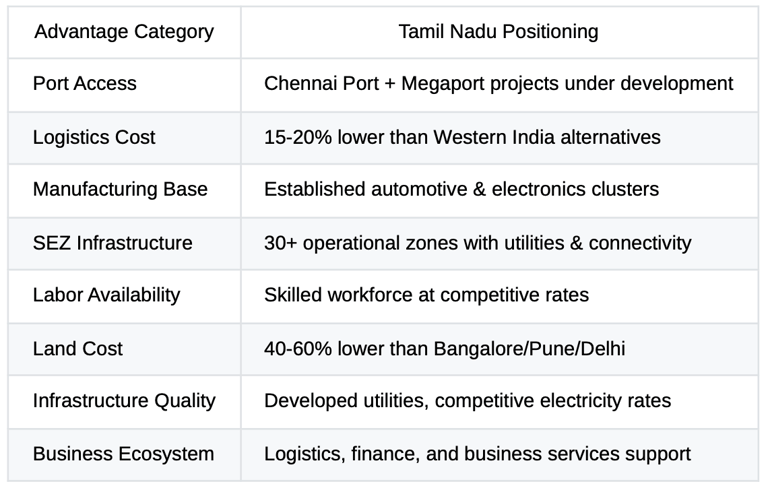

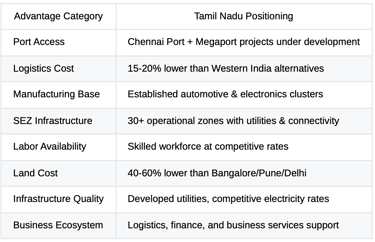

Tamil Nadu's Strategic Position

Among Indian states, Tamil Nadu offers specific advantages that position it as a primary target:

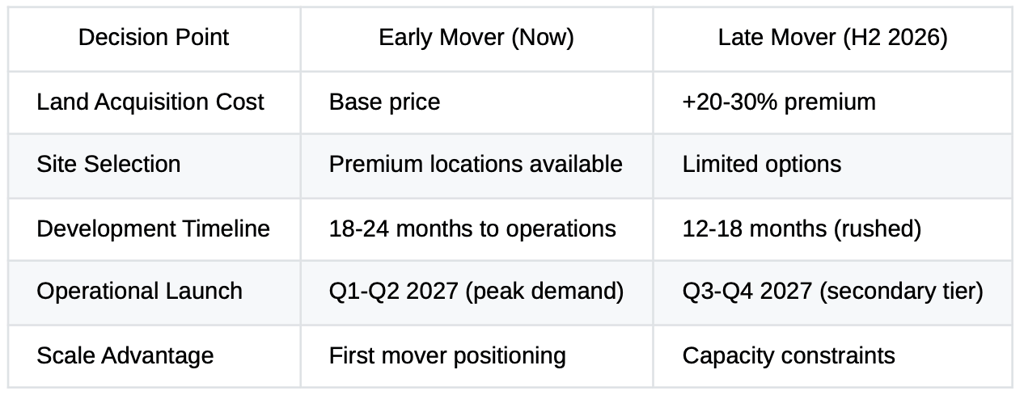

The Investment Timeline Opportunity

Here's the critical insight for industrial investors: the November 2026 tariff deadline creates a compressed but

meaningful planning window.

Timeline to Execution:

Now to April 2026: Land acquisition phase (6 months)

May 2026 to October 2026: Infrastructure development and facility construction (6-18 months)

November 2026 onwards: Operational and scaling phase (2027+)

Why This Matters:

Early movers securing land in late 2025/early 2026 will achieve operational status in 2027, precisely when China+1 strategies mature and demand peaks.

Investment Decision Framework:

What Companies and Investors Should Do Now

For Industrial Investors

The 12-month window until November 2026 presents a unique opportunity to acquire premium industrial land in Tamil

Nadu before supply chain diversification accelerates dramatically.

Priority Criteria:

Port proximity and logistics connectivity

Existing manufacturing clusters (automotive, electronics, textiles)

Sufficient contiguous land for phased development (10-50+ acres)

Access to skilled labor and service ecosystems

Zone status (SEZ, manufacturing hub, or port-based industrial estate)

For Supply Chain Professionals

Use the stability period through October 2026 to execute China+1 site selection and start facility development. The

combination of lower tariffs (47% vs. 57%) and known renewal date provides planning clarity for 18-24 month execution

timelines.

Key Actions:

Identify target regions and facilities

Engage with state governments on incentives and support

Secure land through forward agreements

Begin architectural and engineering planning

For Policy Advocates

The trade data shows India is already benefiting from supply chain diversification. State governments should continue

prioritizing SEZ infrastructure development, port logistics connectivity and skills development programs.

The Longer View: Structural Change, Not Temporary Adjustment

The October 30 agreement represents a tactical pause, not a resolution of underlying US-China competition. Strategic

rivalry over technology access, critical resources, and long-term supply-chain leadership remains firmly entrenched. Even

with the current tariff rate at 47%, the trade relationship remains elevated versus pre-2017 levels.

Supply chain diversification has passed the point of reversal.

Whether the US-China relationship stabilizes or re-escalates, India's role as an alternative manufacturing hub is now structural, not cyclical. This translates to sustained demand for manufacturing and logistics infrastructure over the next 3-5 years, regardless of which scenario materializes in 2026.

Key Takeaways

The October 30, 2025 Trump-Xi agreement reduced tariffs from 57% to 47% and suspended escalation until November 10, 2026

China successfully diversified exports to ASEAN (+12%) and EU (+7%), offsetting US market decline of -15.5%

US import dependency remains concentrated in electronics, textiles, toys and semiconductors vulnerable to future escalation

Three scenarios for 2026: Base case extends stability (60% probability); renewed escalation moderates growth (25%);

full escalation triggers disruption (15%)

The 12-month window creates urgent but manageable planning horizons for supply chain relocation

Tamil Nadu offers specific geographic, economic and infrastructure advantages for capturing China+1 manufacturing investment

Industrial land demand will remain elevated regardless of November 2026 outcome, creating sustained investment

opportunity

Early movers acquiring land by April 2026 will achieve operational status in 2027, coinciding with peak supply chain

diversification demand

The October deal buys time. Smart investors and companies use that time to prepare for whatever comes next.

About VirtueVista

VirtueVista identifies premium industrial, warehousing and logistics land opportunities across India, with particular focus

on high-growth markets like Tamil Nadu. We help investors, developers and multinational corporations navigate the

infrastructure and supply chain transformation reshaping Indian manufacturing.

Ready to discuss supply chain-driven industrial land opportunities in Tamil Nadu? Let's connect.

Email - care@virtuevista.in | Phone Number - +91 74188 75037

Home | About us | Services | Invest With Us | Research | Contact Us

CIN:U68100TZ2023PTC029152 | GST:33AAJCV5804H1ZB

169, Navaladi Building, G.V.Residency, Coimbatore - 641028